Evolution 2: Global offerings and foreign investors

A Look into the Evolving IPO Landscape in Japan — Part II

While the majority of startups outside of Japan have been getting their exits via mergers and acquisitions (M&A), most startups in Japan exit by IPO, or going public. And 2021 was the year in which we witnessed some major changes in Japan’s IPO market.

Background

- Before the global financial crisis hit in 2008, Japan’s IPO would see at least 100 listings each year. After a long period of gradual recovery, 2021 became the first year Japan’s IPO market racked up more than 100 IPOs since the crisis.

- Japan’s major stock exchange, Tokyo Stock Exchange, has a number of boards: the First Section, the Second Section, Mothers, JASDAQ, and TOKYO PRO Market.

- Mothers is the most popular board for high-growth startups. In 2021, some 93 companies went public on Mothers, a record high since the launch of Mothers in 1999.

Source: Tokyo Stock Exchange

Evolution 1: Cornerstone investment (Anchor investment)

Cornerstone investment* has become more popular in Japan since 2021. To learn more about it, please refer to Part I of this series.

“※Cornerstone investment (also known as anchor investment): An agreement by an investor, usually a large institutional or sovereign investor, to subscribe for a fixed monetary amount of shares in an IPO.”

Evolution 2: Global offerings and foreign investors

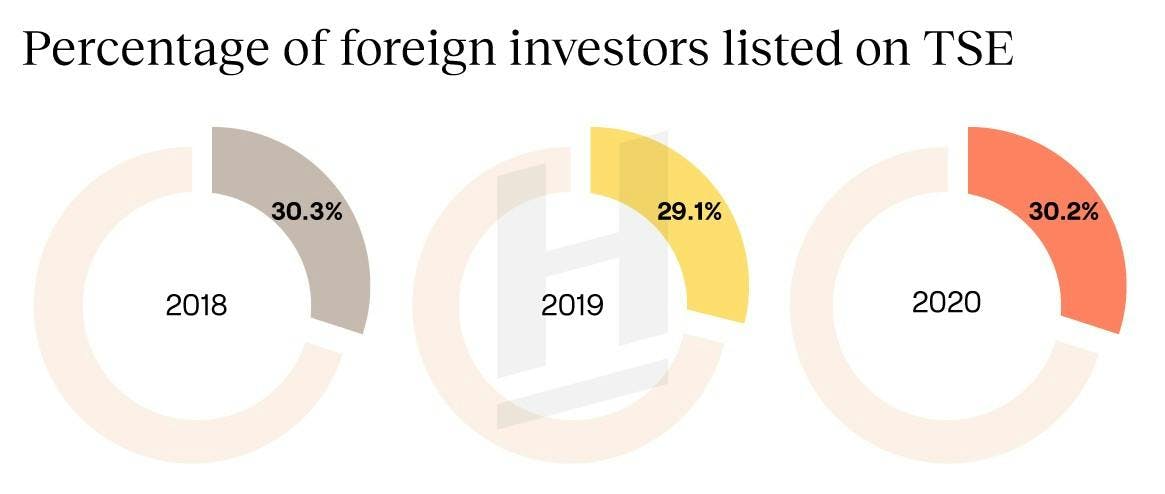

Among the investors that invest in companies listed on the Tokyo Stock Exchange, about 28~31 percent are foreign investors. Specifically, in 2018, 30.3 percent were foreign investors; in 2019, it was 29.1 percent, and in 2020 it was 30.2 percent. The number in 2021 has yet to be announced, but it is likely to be even higher than that of 2020.

Percentage id foreign investors listed on the Tokyo Stock Exchange

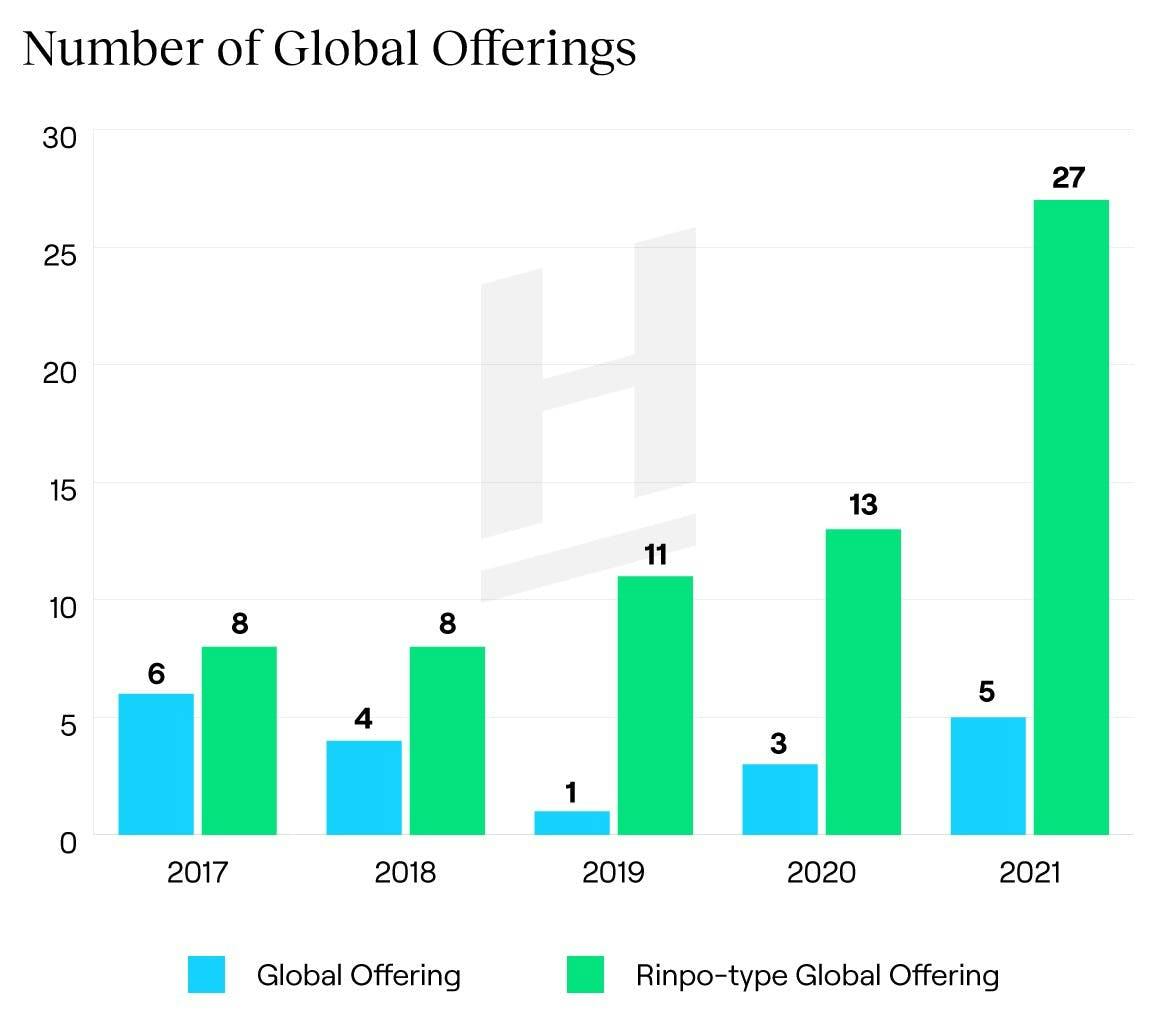

More and more Japanese companies have taken on the challenge to try to attract international investors at IPO, using either Global Offering or Rinpo-type Global Offering.

“※Global Offering: Under this structure, the company and its underwriters need to prepare all the necessary documents and follow the legal processes in each country to be compliant with local regulations. The pro is that the company can raise funds from investors in any country, but the con is that the cost is high and the process is time-consuming.

※Rinpo-type Global Offering: With this structure, the company and its underwriters are able to just use the documents they had already created for the Japanese investors to pitch to international investors. The pro is that it is much easier and less complicated than Global Offering, but the con is that most international investors cannot read Japanese materials and tend to show less interest in companies that cannot afford Global Offering. In addition, there are also a number of other legal restrictions.”

Prominent cases of Global Offerings and Rinpo-type Global Offerings in 2021

We also see an increase of international investors who have invested in the pre-IPO rounds of Japanese companies. Below are some notable examples:

- Photosynth, which raised pre-IPO funding from Fidelity.

- SmartHR, which raised pre-IPO funding from Light Street and Sequoia.

- Net Protections, which raised pre-IPO funding from MY Alpha.

An increasing number of foreign investors are becoming interested in investing in pre-IPO and IPO companies in Japan. Perhaps the change was due to the Chinese government tightening its reins on the nation’s tech industry, leading to restrictions for those who had previously invested in China and consequently pushed them to reconsider Japan. It could also be because the Tokyo Stock Exchange has loosened its regulations on cornerstone investments in the IPO market. Maybe, due to quantitative easing by the US and many European countries, there has a surplus of risk money that both institutional investors and retail investors had to deploy. To sum it up, it was a good year for Japanese companies to go public.

We will be discussing Market Cap, IPO size, and PS ratio, and SPAC, the restructuring of boards in the next two evolution stages. Stay tuned!

Subscribe to our newsletter and stay up to date with all the latest Headline Asia news.

HAS001