Landscape Map: The Rise of Vertical Biz Management Software

This is part 4 of a 6-part series on the trends that are changing Software-As-A-Service (Saas) for Small & Medium Enterprises (SMEs):

🛒Trend #1: Shopify’s growth creates new markets

🍉Trend #2: Restaurants fight for independence from delivery and discovery platforms

👋 Trend #3: Work, reinvented

👔 Trend #4: The rise of vertical biz management software - Below

🤴 Trend #5: HR made simple(r)! - NOV 23

👹 Trend #6: Bookkeeping becomes understandable - DEC 2

If you'd like to have your company featured in this article, feel free to reach out! We would love to hear from you.

Intro: Improving Offline Ops is Tough

Improving SMEs' offline operations is a daunting task across the board: The areas in need of digitization vary across individual industries and technology stacks.

Overall, generalist solutions struggle to match the expectations of certain niche industries. As a result in recent years, we have observed the rise of verticalized software platforms that are targeting specific industries with their offerings.

Vertical software platforms can be defined based on three core criteria:

(1) they provide tailor-made features the fulfill the needs of a specific industry. For example, Shopmonkey (US, part of our portfolio), an auto-repair shop software, goes as far as providing a multi-point inspection management interface for cars, message templates with customer and vehicle statuses, labor hours for specific vehicle parts, and managing diagrams for certain procedures (together with a number of other features required in the auto-repair shop industry);

(2) they bundle different features that you'd expect to find in CRMs like Hubspot, workflow management solutions like Asana, and calendar interfaces like Google Calendar, customer marketing solutions like Mailchimp, or a point of sales like Micros in a single industry-specific hub;

(3) they provide their software through a lean and easy-to-access interface, as oftentimes these software businesses' end clients are mom-and-pop shops that are not particularly tech-savvy.

For a long time, VCs considered these solutions too niche. But the success of companies like Procore (US) in construction, Squire (US) in the barbershop industry, and the abovementioned ShopMonkey (US) have proven that it is possible to create thriving VC-backed companies that focus on specific verticals. Below, we try to try to map this landscape.

All-in-one barbershop platform: Squire's homepage

1. Business Management Software:

- Construction: Procore (US), Vertuoza (Belgium), Graneet (France), Meisterwerk (Germany), PlanRadar (Germany)

- Estate agency: Appfolio (US, Headline portfolio) GoodLord (UK), Innago (US), Sweep Bright (US)

- Wellness: GlossGenius (US), Wavy (France), Square (US)

- HVAC technicians: Service Titan (US), Zuper.co (US), HouseCall Pro (US, Headline portfolio)

- Auto repair: Shopmonkey (US, Headline portfolio) CarServ (US), Autoleap (US)

- Hospitality: CloudBeds (US), Mews (UK), Hotel Manager (UK)

- Gym and fitness: Sindro (US), PlayMetrics (US), Glofox (Ireland), Heja (Sweden), PerfectGym (Poland)

- Care & Health: Digitail (Spain), Doctorly (Germany)

- Tours: Checkfront (US), Fareharbor (US, acquired)

- Education: Klassroom (France)

- Retail: BrightPearl (UK)

The landing page of Appfolio, a property management solution

Having worked alongside the likes of Appfolio, HouseCall Pro, and Shopmonkey we have noticed firsthand some traits that allow these businesses to thrive:

(1) The founders have an in-depth understanding of the pain points specific to their customers' industries. The founders leverage their industry knowledge to focus on pain points that they have either personally experienced or discovered when trying to engage with that industry. Service Titan (US, raised 399M$), a service management platform used by HVAC technicians, was built by two founders whose parents were working in the service industry. Similarly, Vertuoza (Belgium), a construction management platform and suite comes from a founder who was previously the CEO of a construction company.

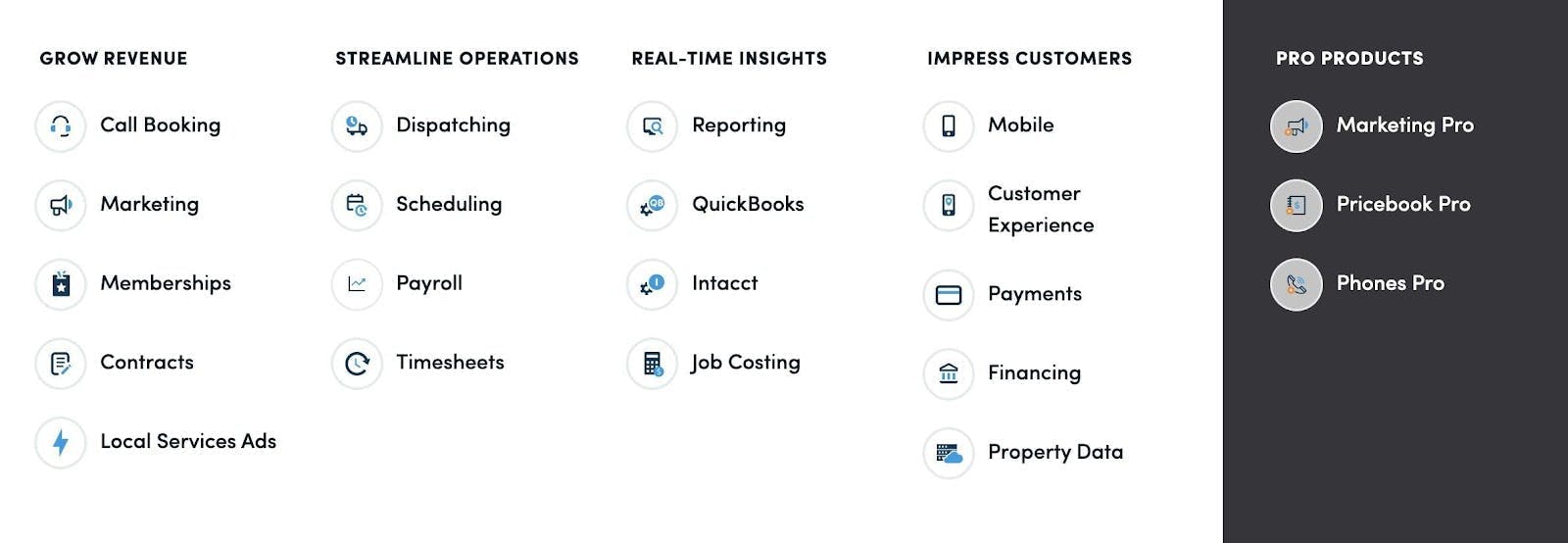

(2) Their products bundle an increasing number of features over time. This development is a byproduct of these verticalized solutions becoming increasingly integrated with the everyday processes and technology stack of their end clients. For example, Service Titan has gone on to develop payroll features and wants to integrate their solution with their client’s payment stack. Customers are receptive to replacing third-party solutions with something that is better integrated with their main business management software. And, it allows these business management solutions to monetize different features. See below:

ServiceTitan's product features

(3) Adoption is a major challenge. In most cases, these companies are providing software to end clients in industries where digitization is still limited.

More generally, the profile of these end clients can be categorized at mom-and-pop shops, operating in "manually-driven" and highly fragmented markets. This makes onboarding a key - and time-intensive - area.

To drive adoption, these businesses rely on a set of tools: an aggressive sales team, internally developed educational content, local channel partners, and accessible pricing. A byproduct of this, these companies find themselves operating massive customer engagement teams. On average, there is 1 customer support agent for every salesperson - a 3x ratio compared to software companies that focus on enterprise sales.

(4) Subscription is rarely their first source of revenue. The pricing strategy of these vertical software providers is focused on making their solutions financially accessible to their end clients.

In most cases, companies do not charge an onboarding fee, but rather rely on an accessible monthly subscription price. In some cases, the software itself is offered to customers free of charge, in these cases companies monetize via a transaction fee for processing payments, through additional premium features, financial services such as offering loans, or a via a take rate charges on a B2B/B2C marketplace layer.

Financial services are one of the most common and strong sources of revenue for these players. For example, ShopMonkey (US) monetizes its solution with both a subscription fee and a payment-processing fee for its auto-repair management solution. As of today, payment processing represents a bigger share of their revenues than subscriptions.

2. SaaS-enabled marketplaces

SaaS-enabled marketplaces are businesses whose product allows companies or individuals to manage their business or service through a SaaS platform ,0with marketplace features. The platform usually allows them to engage and transact with suppliers, buyers, customers, and/or service providers within their network.

The greatest associated benefit derived from a SaaS-enabled marketplace is proving the end customers with the benefit of engaging in a network of existing sellers and buyers, often the most prominent barrier to entry associated with marketplaces.

⭐ B2C SaaS-enabled marketplaces: Brighter (Sweden, wellness), Docplanner (Poland, raised $140M, doctors), Doctolib (France, doctor), Hemea (France, architecture), Weaver.build (UK, architecture), Fincompare (Germany, Bank), Plentific (UK, housing), Tock (US, restaurants), Mindbody (US, acquired, wellness), Fresha (UK, wellness), Slick (UK, wellness), or Floom (UK, florists) have built solutions that allow SMBs to more efficiently manage their operations.

They function by converting their software users into business partners, who can offer their products and services on their users' existing B2C marketplace. These platforms monetize their network of buyers and sellers through an intermediary transaction fee, often labeled as a payment processing fee.

Independent florists, unite: Floom's landing page

⭐ B2B SaaS-enabled marketplaces: These solutions streamline offline operations and are well-positioned to also offer procurement, to connect freelancers and contractors to SMBs, or manage additional services such as shipping. Xeneta (Norway, freight), Sendify (Sweden, freight), DrayAlliance (US, freight, part of Headline's portfolio) all focus on connecting SMBs with shipping providers. Squire (US, raised 106M$), is a barbershop management software that also functions as a one-stop shop for barbers to order and stock supplies.

Dray Allaince's value proposition for shippers

⭐ C2C SaaS-enabled marketplaces: in the case of C2C platforms all participants are presumed to be equals in any given transaction or interaction. End users tend to be individuals providing or engaging with services to other individuals in communal-based settings. These include services such as individual property selling, online classes, pet sharing, carpooling, and mentorship sessions. In recent years the more prominent C2C SaaS-enabled marketplaces include the likes of LiveMentor (France, education), Studocu (The Netherlands, education) both of which have built solutions to allow individuals to produce their own educational content, sell homework and course materials together with hosting live classes.

Many thanks to Ilan Nabeth for the invaluable research that made this series possible, and to Yusuf Janahi and Anna-Stella Fetha for your contributions!