With higher interest rates making capital more expensive, the term “capital efficiency” or “burn productivity” has been increasingly thrown around in the startup and venture industry. There are many different metrics to measure capital efficiency, which try to calculate how much it costs to grow a business. In other words, for every dollar a business burns, how much does it grow as a result?

Why it matters?

At Headline, we define capital efficiency by dividing the net annualized gross profit growth (net ARR growth x gross margin) by the net burn of a business in a given period. We like to look at growth on a gross-profit basis to more accurately compare the growth of a low-margin e-commerce business like Sonos or GoPuff with a high-margin SaaS business like SEMRush or Appfolio. Within this framework, businesses should operate at a capital efficiency of at least 0.5. This means that for every dollar a business burns in a given period, it should grow the annualized gross profit by 50 cents. Note that for a high-margin SaaS business, this correlates to a “good” burn multiple.

We at Headline have been hawkish about the attainment of 0.5+ capital efficiency because a business's capital efficiency directly drives shareholder value creation and destruction. Why should operators and founders care about that? At the exit, the largest shareholder group is usually the founders and their team.

In the following, I will walk through a basic financial model to illustrate why we believe a capital efficiency of 0.5 or higher is optimal for shareholder value creation, and a capital efficiency of below 0.5 starts to increasingly eat into the value creation of a business. You can find this model for your reference in this GSheet.

The Model

Let’s assume a typical SaaS business generates $1M in ARR with a gross margin of 75%. This company will grow well, compounding 10% month over month and achieving over 2x year-on-year growth! We will assume the business raises its first round of financing, a $5M round on a $25M pre-money valuation, resulting in ~17% dilution to the founders.

From there, we make two assumptions:

- The business will operate at a constant capital efficiency, meaning it will grow its annualized gross profit at a set rate for every dollar it burns.

- Every time the business runs out of money, it will raise 18 times the last month’s burn at a certain gross profit multiple, effectively 18 months' worth of runway based on the latest month’s burn.

Assuming a capital efficiency of 0.5 and a gross profit valuation multiple of 10x, the business would burn $45M, ending 2023 with $31M of ARR and creating $110M in shareholder value for the founders based on the dilution.

If we now assume one small change – that the capital efficiency is 0.4 - and a gross profit multiple of 10x, you can see that the business would now burn $56M, ending 2023 with $31M of ARR. The equivalent shareholder value created for founders would be $92M - almost $20M less than at a capital efficiency of 0.5.

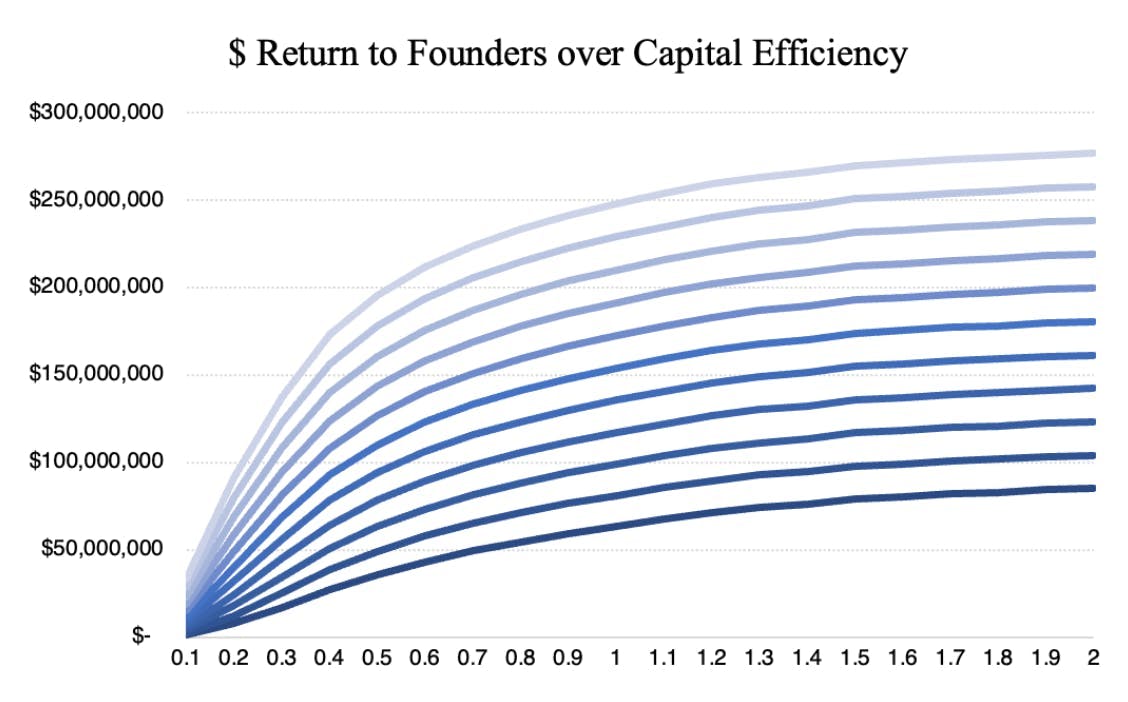

Based on this model, I created a data table that runs various scenarios based on the capital efficiency at which the business operates and the gross profit multiple. In the graph below, I chart out the dollar returns to founders over the assumed capital efficiency; each data series represents a given gross profit multiple. The lightest data series at the top reflects a 15x valuation gross profit multiple and returns the most to founders. The darkest data series assumes a 5x valuation gross profit multiple and the least amount of value to founders.

The chart clearly shows that the greater the capital efficiency of a business, the greater the dollar return to founders and shareholders. The impact is significant. Also, the highest valuation multiple naturally gets the greatest return. Nonetheless, a business operating at a capital efficiency of 0.2 with a 15x valuation multiple does not create a greater return to founders than a business with a 5x gross profit multiple at a capital efficiency of 1. A business can be valued at a third of a multiple compared to another business and still create as much shareholder value for the founders simply by operating more capital efficiently. A business operating at 2 versus 0.2 will return about ten times the amount to the founders.

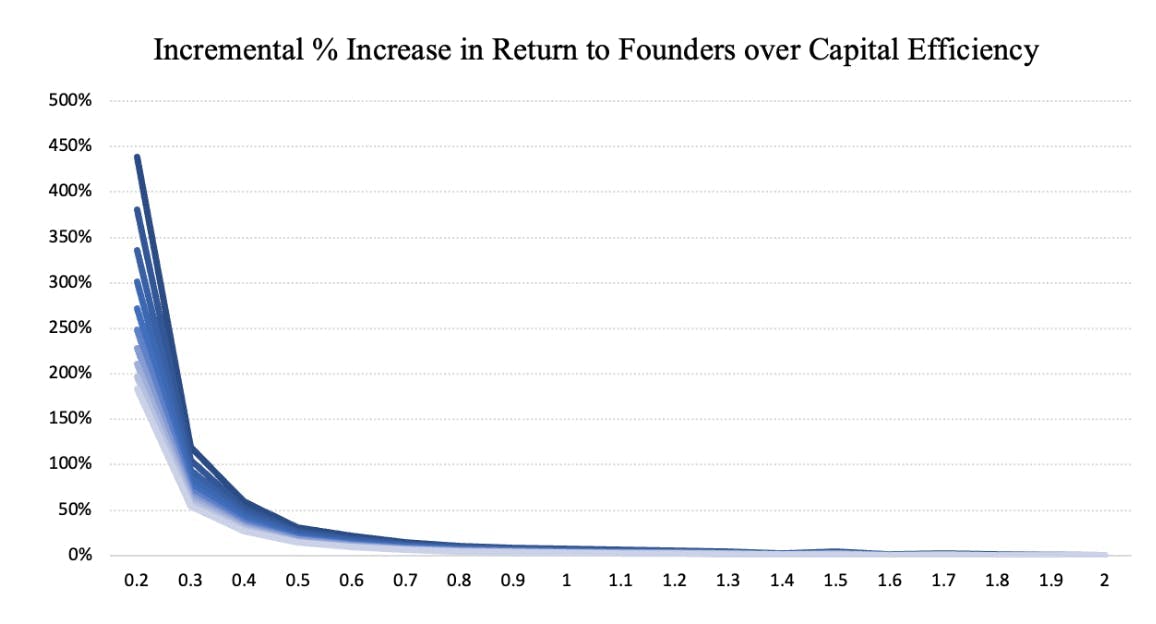

Nonetheless, the return of each data series flattens the greater the capital efficiency gets. In other words, for every decimal point at which the capital efficiency of a business increases, the less the increase in dollar return to founders. To better visualize this, in the chart below, I mapped out the incremental percent increase in return to the founders based on each decimal increase in capital efficiency of a business. Each data series represents a different valuation gross profit multiple, ranging from 5x at the darkest to 15x at the lightest data series.

This graph shows that the most significant increase in dollar return to founders is in the early decimals of capital efficiency increases. For example, the largest increase comes from a business operating at a capital efficiency of 0.2 versus 0.1. A business operating at a capital efficiency of 0.2 versus 0.1 will generate 200% to 400% greater returns to founders at exit, depending on the gross profit multiple.

In Summary

The greater the capital efficiency becomes, the lower the incremental percentage increase in return to founders. The decrease of this dynamic is exponential. From 0.7 onwards, increasing capital efficiency by one decimal increases the return to founders by less than 10%, regardless of the valuation.

With this chart, I wanted to show why we like to see businesses operate at a capital efficiency of 0.5 or above. Up from the 0.5 mark, the incremental % increase to founders and all shareholders is 25% or greater–which is very significant!

The natural question for founders is: How do I financially engineer my business to grow at a capital efficiency of 0.5 or higher? Beyond having found product-market fit, we at Headline see the primary dynamic for this growth as the customer acquisition cost payback period of a business. If you’re looking to connect about ways to increase your capital efficiency, email me at Nicolas von Blottnitz nicolas@headline.com.

In my next article, I will cover why Headline believes a payback period of around 12 months is ideal for most businesses. Stay tuned.