As a consumer, you may have noticed that more and more non-financial-service companies start to provide debit cards or credit cards. Recently, brands like Apple, Uber, DoorDash, Instacart, and even sports teams, have jumped on the card issuing-band wagon. If you have used any of these services, it’s very likely that you‘ve benefited from the emergence of Card-as-a-Service.

Embedded Finance Part III: Card-as-a-Service

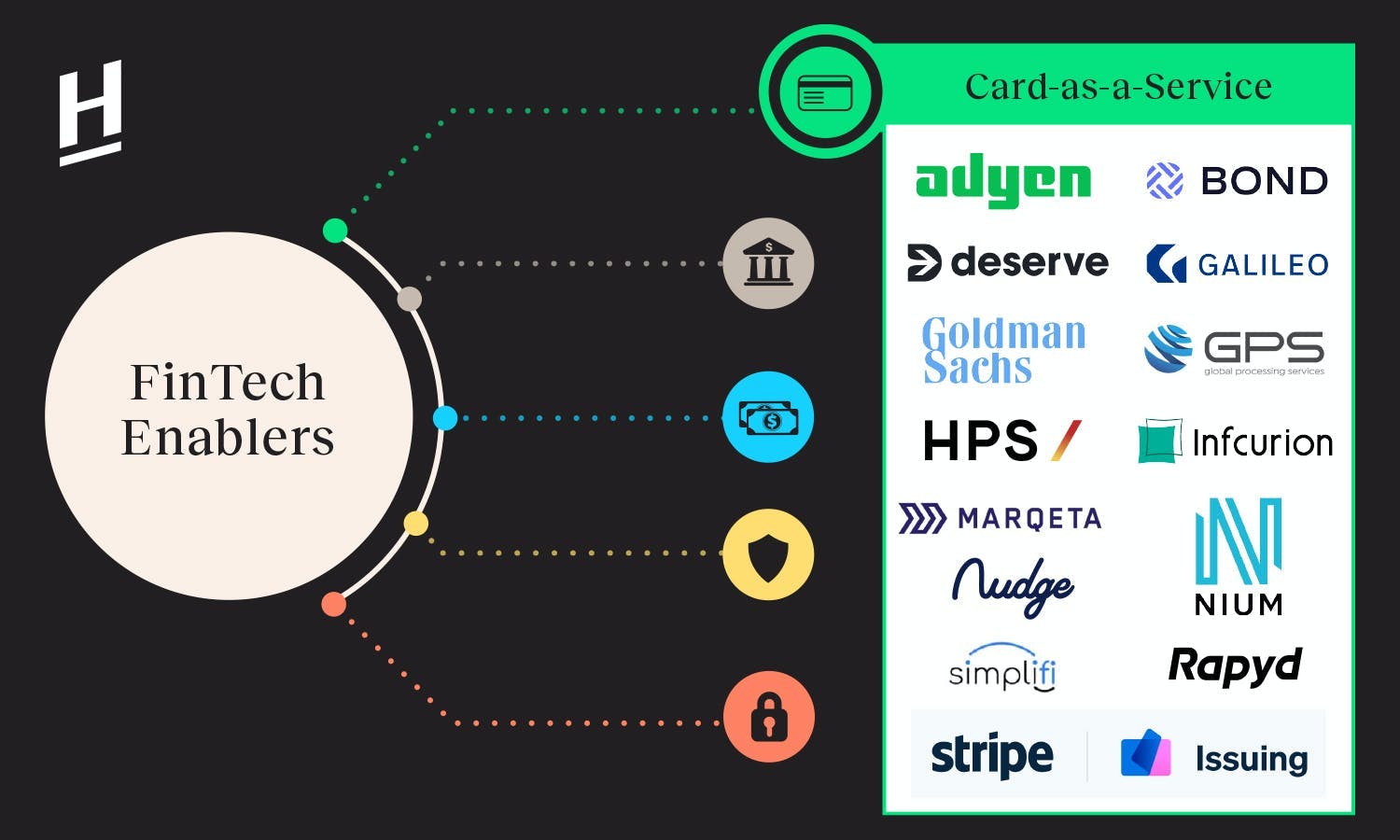

FinTech enablers

What is Card-as-a-Service?

The concept of white-labeled credit cards or partnership credit cards isn’t new at all. Plenty of department stores have them, but the most well-known use case for these partnership credit cards is probably airline companies. Their cards are usually developed and powered by traditional banks such as Citibank or MasterCard. However, every time an airline company wants to issue a new card with a new kind of screening process, limitation, or rewards, it needs to renegotiate terms with issuing banks, hammer out the details, and build out everything from scratch. The process usually takes two years.

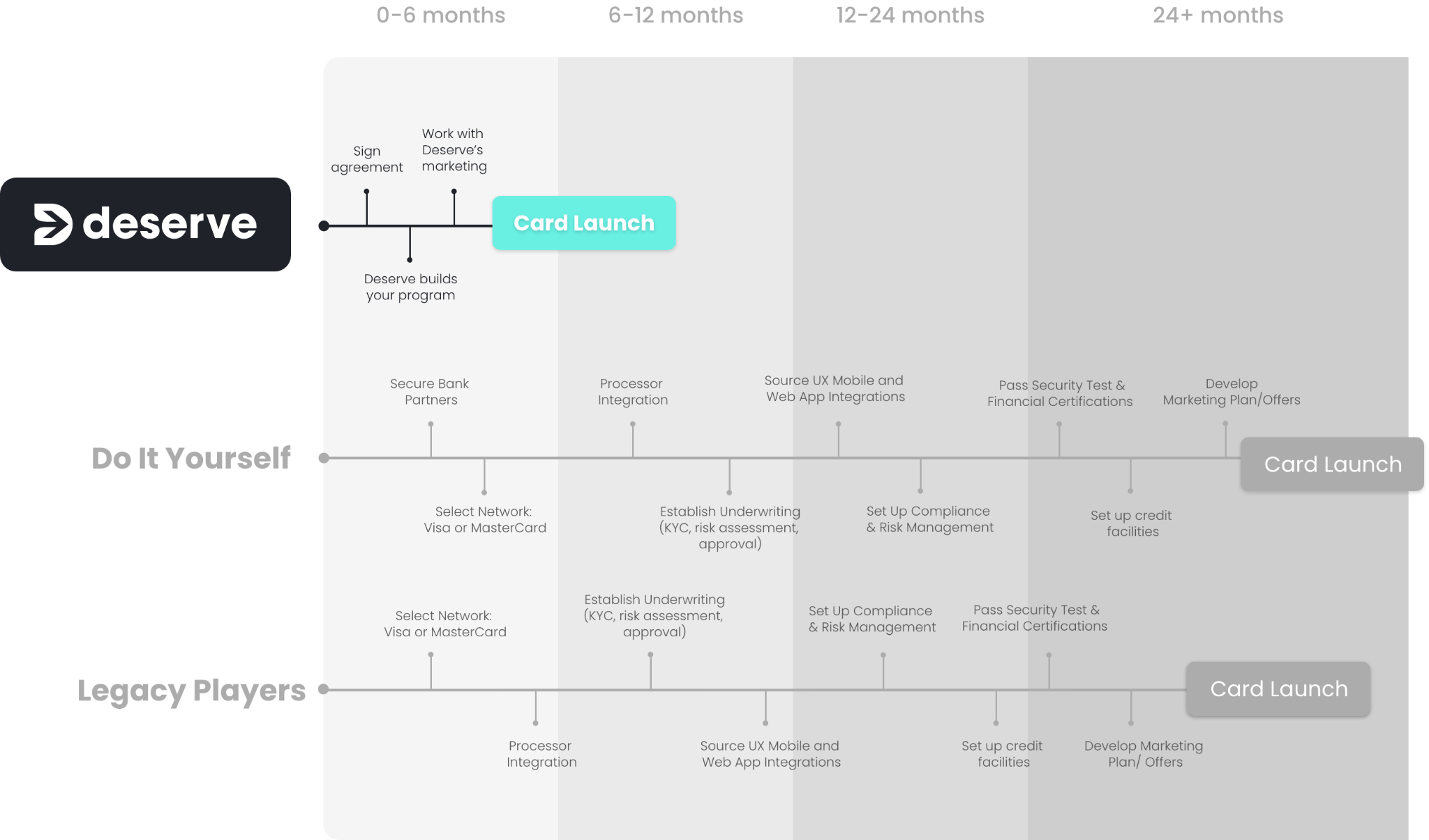

Image courtesy of Deserve

The new Card-as-a-Service players are different from the traditional banks mostly in speed, thanks to API. One Card-as-a-Service company, Deserve, breaks down the timeline for clients interested in issuing their cards with a CaaS company, working with traditional banks, or DIY-ing the process.

CaaS companies do a great job streamlining the process for their clients. They help their clients with origination, underwriting, bank and bureau integration, customer service, compliance and risk management, etc. Simply put, Card-as-a-Service companies provide a comprehensive, top-to-bottom solution: from determining which customer is eligible for a credit card to how much interest rate should be charged on loans, from how to create the physical card to how to deal with KYC/AML and fraud.

CaaS is paving the way for the future of non-financial service cards.

Pure-Play Card Issuance Enablers

- Marqeta: Established in 2010 in the US and went public on NASDAQ in 2021 with an initial market cap of $15B. Marqeta is the enabler behind the curtain that helps DoorDash, Uber, and Instacart to issue their cards. Marqeta’s offering enables partners to quickly launch debit/credit cards with flexible controls, including the ability to turn on or turn off parameters with minimal friction, such as annual percentage rates, rewards, and credit lines in real-time based on custom rules. It lets its partners access dashboards instead of legacy spreadsheets, along with capabilities to activate users instantly and embed cards into digital wallets

- Cardless: Established in 2019 in the US and backed by Greycroft, Cardless is targeting a different client base. Most of the Card Issuance Enablers serve digital-native platforms such as Uber and DoorDash or the big tech companies such as Apple and Square. Yet, Cardless’s major clients are sports teams, such as Manchester United, Cleveland Cavaliers, and Boston Celtics.

- Nudge: Established in 2020 in Japan by serial entrepreneur Okita-san, Nudge can allow any influencer, KOL, creator, or celebrity to issue their credit card with their own branding and card rewards. Headline Asia is proud to invest in Nudge as a lead investor in its last round. Check out our interview with Takashi Okita, the CEO of Nudge.

Stock photo of a Bank Card

Expansion from Banking Enablers or Payment Enablers

- Banking Enabler: We previously introduced the concept and the major players in the field of Banking Enabler, AKA Banking-as-a-Service. Most of them do not just provide the savings account, but also card issuance as part of their offering. The Banking-as-a-Service players who also help issue cards are Solarisbank, RailsBank, Synapse, etc.

- Payment Enabler: Some companies started as helping SMEs or larger companies with their B2B payments and realized their clients all want to issue their cards with their own branding. The notable players are Rapyd, Issuing by Stripe, Adyen, BOND, and Nium.

- Nium: Established in 2015 in Singapore, Nium is the first B2B payment unicorn from Asia. Nium helps companies accept and make B2B payments as well as issuing their own cards. It has just recently raised $200M in 2021 and has issued more than 30 million cards with card issuance licenses in more than 11 jurisdictions. Nium is also known for acquiring Wirecard’s business in India.

Traditional banks and Financial Institutions

Similar to the landscape of Banking-as-a-Service, the incumbent financial institutions that can react fast enough to the new trend are staying competitive to the startups.

- Goldman Sachs: The most famous use case of a big tech company utilizing Card-as-a-Service might be Apple Card, which is powered by Goldman Sachs. At first glance, this looks like an old-fashioned white-labeled partnership, but Goldman Sachs actually builds out a modern system with advanced API. They announced that they’re seeking to replicate the Apple card model with other companies they’re working with.

Apple Card

The Bigger Picture

Card-as-a-Service, or Card Issuance Enabler, is just a fraction of the bigger trend of Embedded Finance, AKA FinTech Enablers. If you want to learn more about FinTech Enablers, check out our Intro to FinTech Enablers and Embedded Finance.