Some Lending-as-a-Service providers can approve your loan in a matter of minutes.

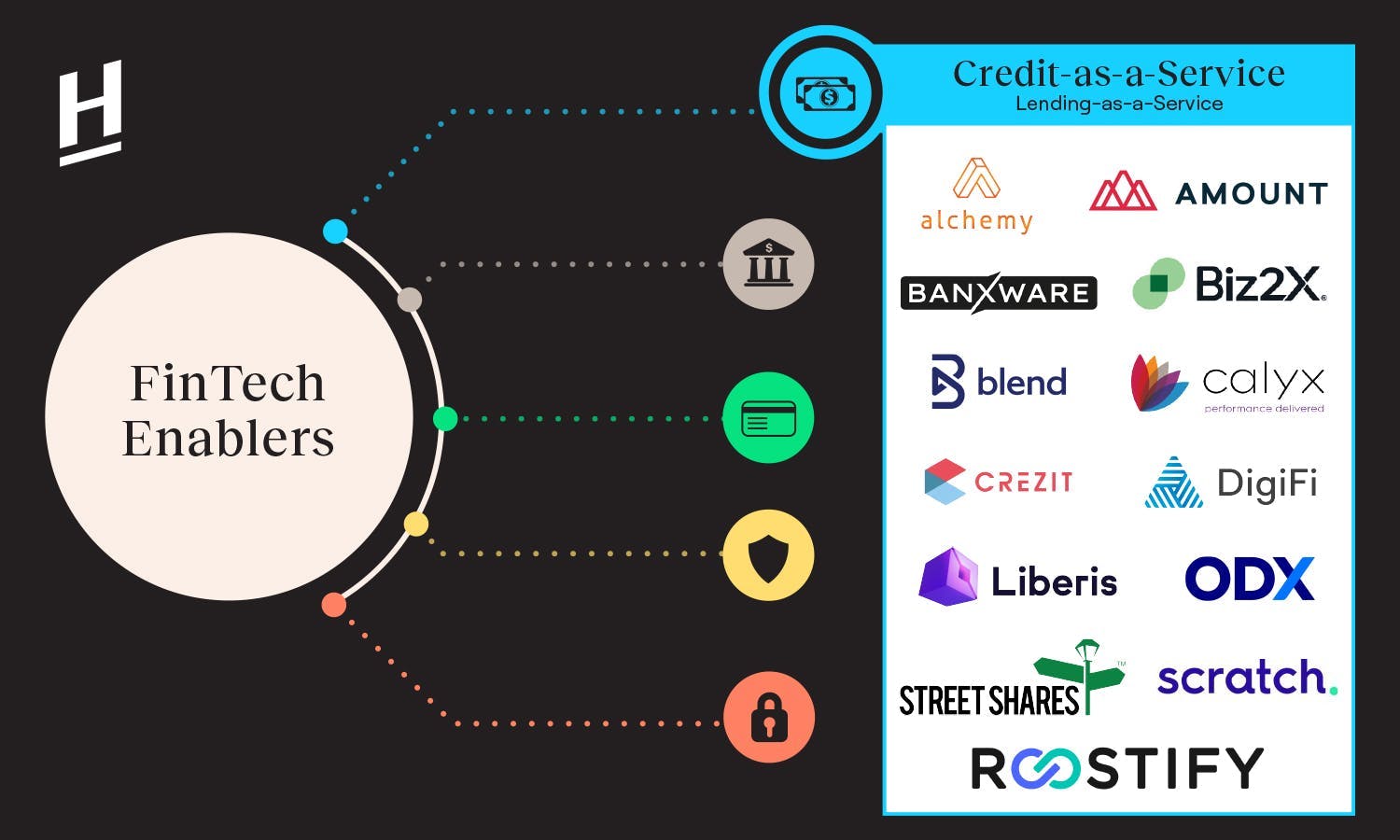

Embedded Finance Part IV: Credit-as-a-Service

In the past, all financial services were provided by traditional financial institutions. However, that’s not the case nowadays. There is an emerging trend where financial services are being created by a FinTech Enabler, and then distributed by a client company — and oftentimes, these companies that are doing the distribution aren’t even remotely a financial institution. (If you’re curious to know more about FinTech Enablers, we do an overview of the concept here.)

Continuing our series about FinTech Enablers, AKA Embedded Finance, this piece will focus on how lending service is embedded into other services.

What is Credit-as-a-Service?

Also known as Lending-as-a-Service and Embedded Lending, Credit-as-a-Service enables companies to provide loans. Providing a lending service involves the process of credit scoring, credit underwriting, fraud detection, loan disbursement, and repayment collection.

The providers of Credit-as-a-Service are companies that take care of credit scoring, credit underwriting, and fraud detection for their clients, while their clients will be in charge of marketing the service, attracting borrowers, disbursing the loan, and collecting the repayment.

Advantages of Credit-as-a-Service

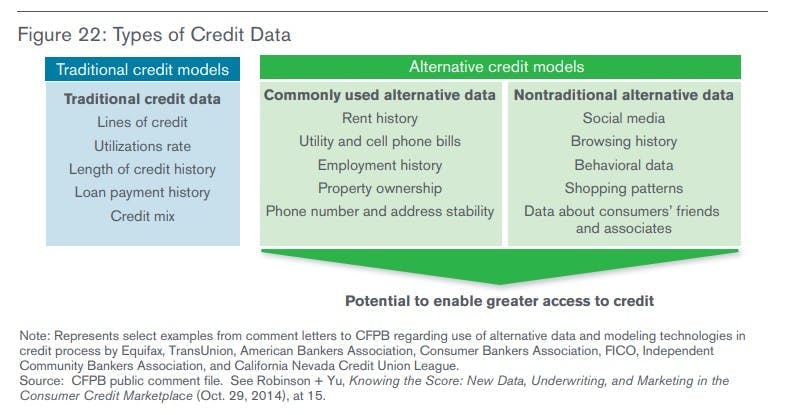

One of the advantages of Credit-as-a-Service is that it provides alternative data. In most cases, the clients are companies that have collected enormous amounts of data from their customers, and Credit-as-a-Service providers come in to help figure out how to utilize such data to determine how credit-worthy the customers are.

Those data, AKA alternative data include online behavior, activities on social media, call records, subscriptions, etc., which are not the data that the traditional banks and financial institutions use for their credit scoring.

Another great advantage of Credit-as-a-Service is digitalization. Many traditional financial institutions still handle the loan application and credit scoring process using pen and paper. Many Lending-as-a-Service providers are not just helping digital-native clients to provide loans, but also helping traditional banks and non-banks to digitize their lending services.

Notable Players in this field

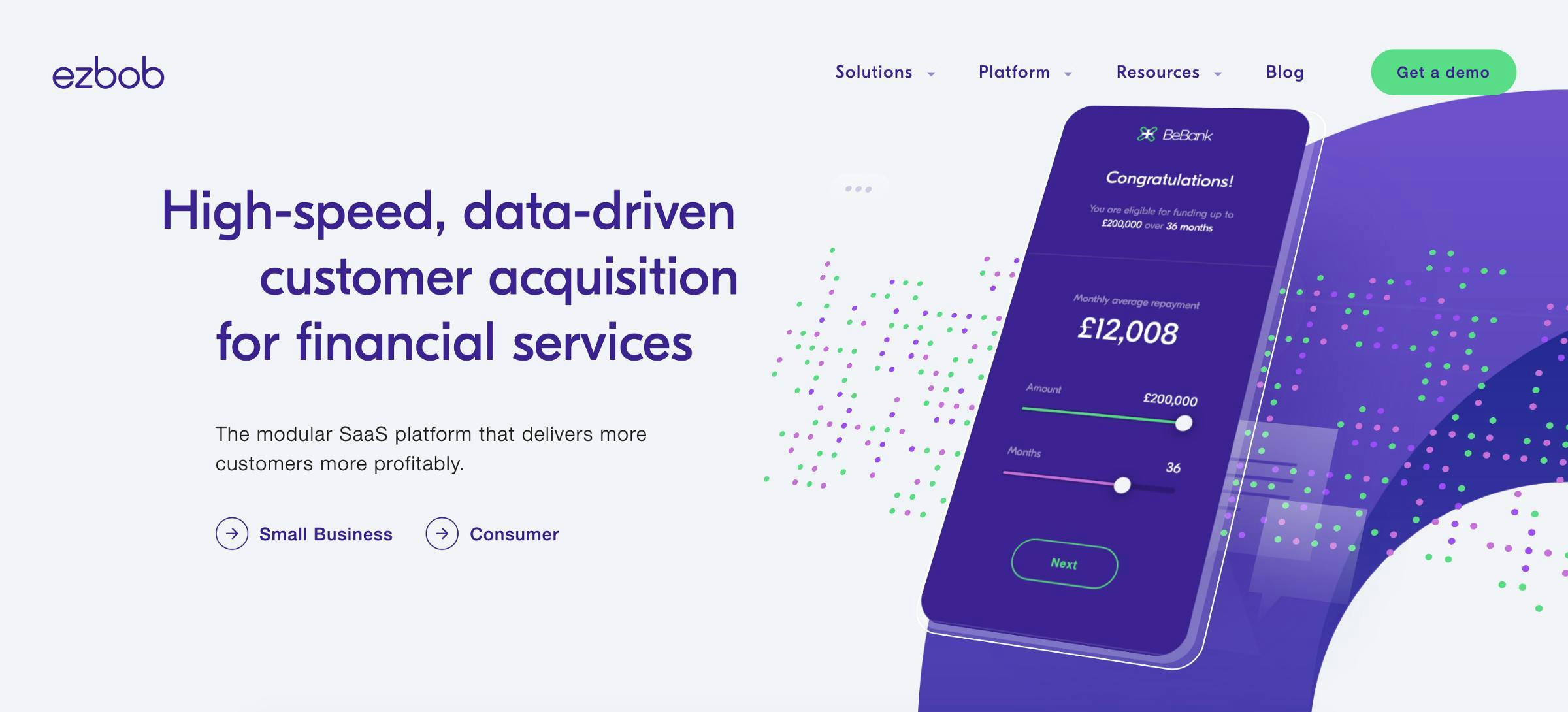

Ezbob: As a pioneer in the rapidly growing Lending-as-a-Service sector, Ezbob started in 2011 in the UK. It offers an open platform that enables financial institutions to build, launch and operate financial products for their customers, drawing on the data-rich open banking environment. They were able to reduce loan-servicing costs by up to 80% and allow SME customers to receive a lending decision in as little as seven minutes with funds transferred on the same day — this made Ezbob a game-changer in the lending sector.

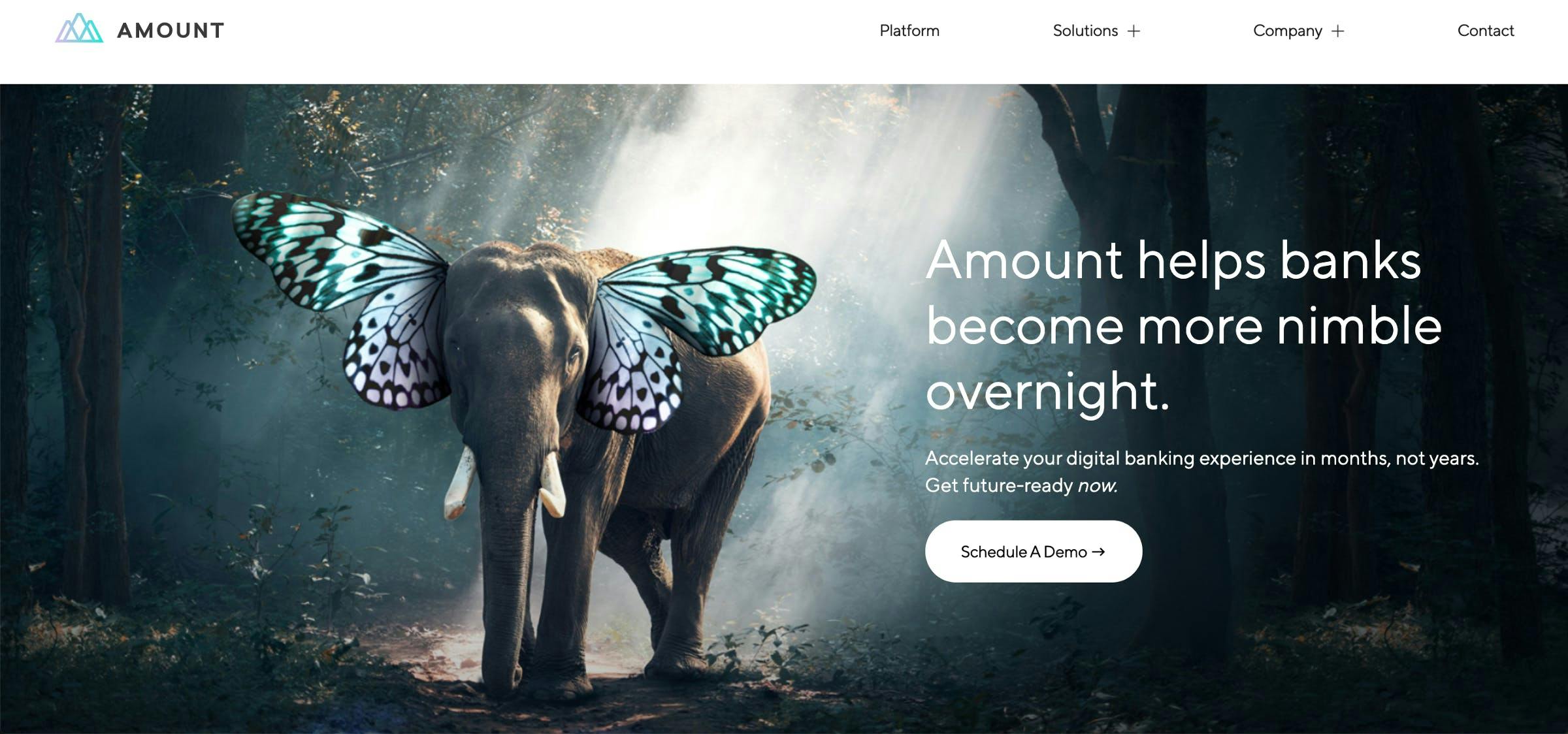

Amount: Established in 2019 in the US, it has become a unicorn in less than two years. Similar to Ezbob, Amount helps financial institutions go digital in months — not years. HSBC, TD Bank, Regions, Banco Popular and Avant are some of Amount’s clients. On the other hand, Amount also enables merchants to offer installment options under their brand. Recently, Barclays US Consumer Bank became one of the first major banks to partner with Amount to provide such a white-labeled installment service.

Liberis: Founded in 2007 in the UK, Liberis has provided over £500 million in financing to 16,000 SMEs across Europe, the U.S., and the U.K. It has then shifted toward B2B2B, now predominantly partnering with marketplaces, software providers, and acquirers, such as Worldpay from FIS and Global Payments. These partners integrate with Liberis to offer personalized pre-approved revenue-based financing to their end customers.

Roostify: Established in 2012 in the US, Roostify is a Lending-as-a-Service company that focuses on mortgage lending. Santander, TD Bank, and Colonial are among its clients, who utilize Roostify’s technology to analyze behavioral data and digitize their mortgage application process.

Linear FT: Linear FT is focused on helping banks reinvent the small business lending process. It provides a unique combination of market-leading software, analytic insights, and professional services to deliver a game-changing digital experience. As a wholly-owned subsidiary of OnDeck (NYSE: ONDK), one of the largest online small business lenders, Linear FT draws on the heritage of USD $10 billion loan over the last decade.

Crezit: Crezit is one of the very few, if not the only, Credit-as-a-Service startup in Japan, which focuses on connecting the traditional consumer loan lenders to the digital native tech companies. Recently, it announced a partnership with one of the largest consumer lending companies in Japan, ACOM.

Embedded Finance Part V: Insurance-as-a-Service

In the past, financial services have always been provided by what we customarily think of as financial institutions — banks, credit card companies, even insurance companies. However, it’s become increasingly common for non-financial companies to become the distributors of financial services, thanks to embedded finance, AKA finance enablers.

Jan 25, 2022

Intro to FinTech Enablers & Embedded Finance

Industries develop over time and when they mature, they tend to become more specialized. That’s what is currently happening with the FinTech industry and financial service in general. It’s entering a new phase of division and specialization.

Jan 25, 2022