In the past, financial services have always been provided by what we customarily think of as financial institutions — banks, credit card companies, even insurance companies. However, it’s become increasingly common for non-financial companies to become the distributors of financial services, thanks to embedded finance, AKA finance enablers. (We talk more about this concept of finance enablers in this article, which also leads to other parts of this series.) In this article, we will be focusing on how insurance products are getting more commonly embedded into other services.

Embedded Finance Part V: Insurance-as-a-Service

Insurance

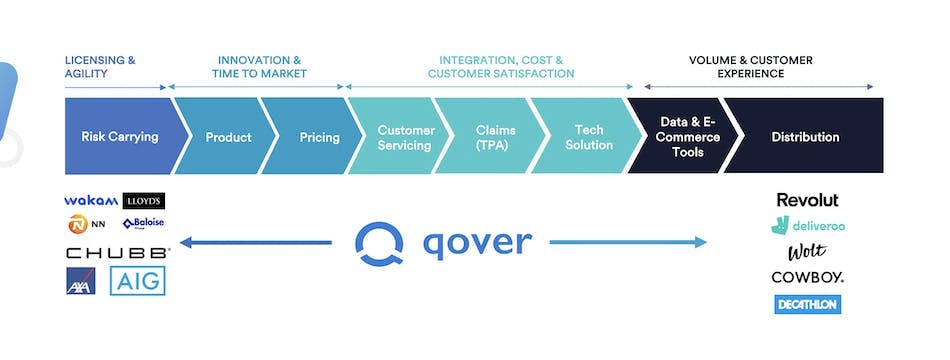

Similar to what we discussed in our article about Card-as-a-Service, the idea of insurers selling insurance products via partners such as airline companies have existed for some time now.

With the emergence of the internet and the popularization of personal-use computers, insurance innovating companies like Guidewire and Duck Creek emerged two decades ago. More recently, InsurTech startups such as Tractable, Concirrus, and Shift Technology have begun to apply AI and Big Data to the insurance industry.

However, since COVID, we have seen a massive increase in the number of early-stage InsurTech enablers and the amount of funding being invested into them. Some B2C InsurTech companies have also spun out their proprietary technology into end-to-end SaaS solutions for other companies to provide their own insurance. One example is ByMiles, which is spinning out By Bits, a customizable usage-based Insurance platform.

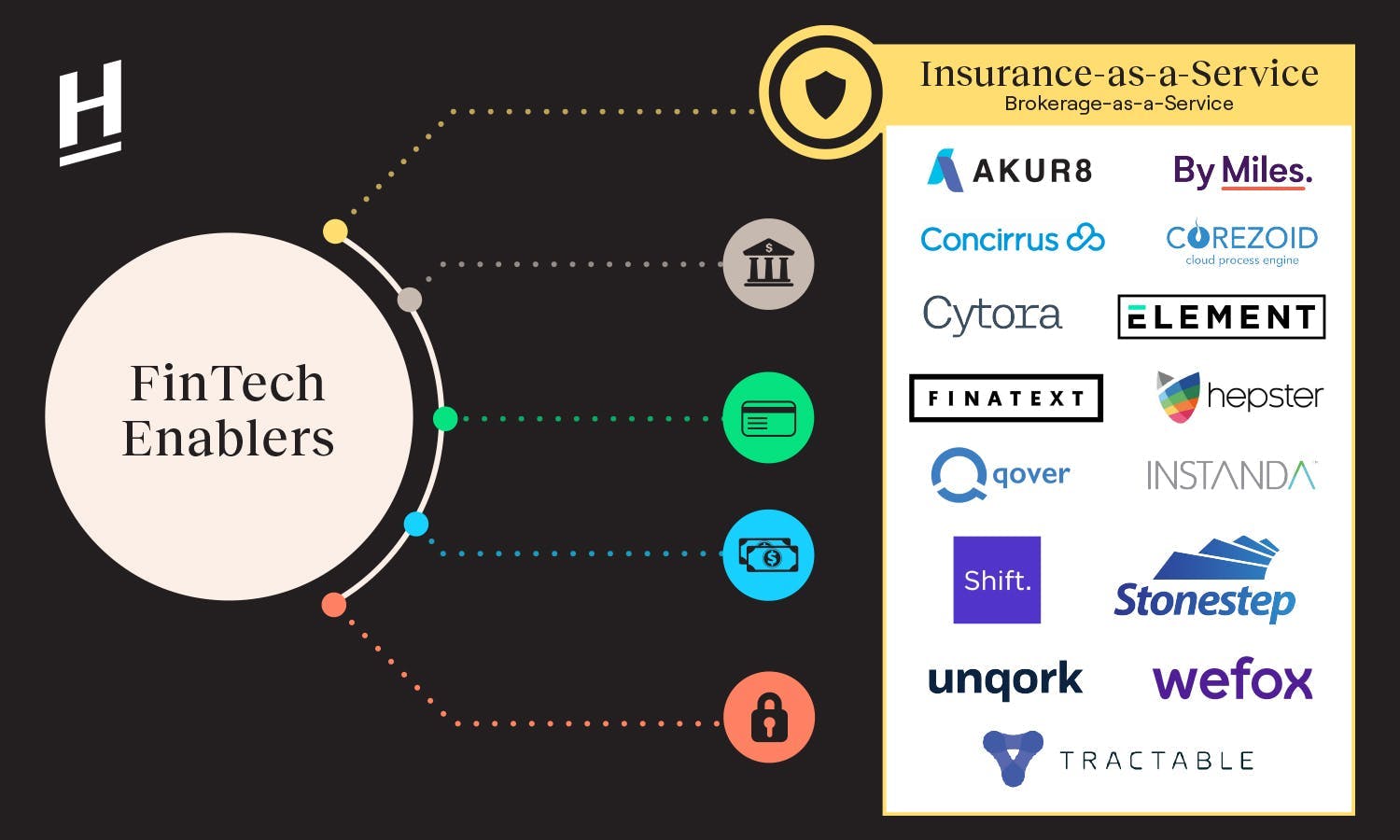

FinTech Enablers

Types of Insurance Enablers

Providing insurance products involves many different layers of work. Below are some angles that Insurance Enablers have chosen to cut it:

- Digitalization and Automation: Efficiency tools that focus on process improvement for the front office, policy or plan management, and claims management.

- Data and Technology: Data analysis services that utilize AI or blockchain technologies to capture or analyze data for specific use cases or across the value chain.

- Full Stack: Startups offering full digital insurance infrastructure to launch insurance products. They are B2B2C or B2B2B-oriented and usually have their own insurance underwriting and distribution license.

Among all the great insurance enablers out there, here are some outstanding ones:

Wefox: Established in 2015, it has raised more than USD $900 million in funding from investors like SBI, Target Global, Horizons Ventures, and Salesforce Ventures. As a full-stack insurance company licensed in Lichtenstein, Wefox can passport its license to other European countries. Yet, it doesn’t sell the insurance itself but instead sells them through 700 local agents and 5000 associate brokers. These agents and brokers’ work don’t only get to sell innovative insurance products, but also get to use the highly digital and automated sales tools that Wefox has developed.

ELEMENT: Incubated in 2017 by Finleap, who also incubated a successful Banking-as-a-Service company called Solarisbank, ELEMENT has raised more than USD $75 million in VC funding. ELEMENT is also a full-stack insurance provider, but it strictly sticks to a B2B2x model. For example, it has enabled real estate companies to provide their own branded household and liability insurance. It has also powered Volkswagen’s car insurance products and other white-labeled insurance such as travel insurance and cybersecurity insurance.

Finatext: Established in 2014, it is one of the very few Insurance-as-a-Service companies in Japan. Among other embedded finance services, Finatext provides “Inspire”, which is a SaaS unified system that can connect traditional insurers to other companies, so that other companies can also distribute insurance products. It provides a user-friendly UI for the customers to apply for their insurance, manages their contracts, and ask for payments. On the other side, it provides insurance companies/agencies with a system console to manage accounts, contacts, and claims from the customers.

Akur8: A developer of an AI-driven insurance pricing platform designed to provide AI-powered pricing automation and optimization for insurance carriers. The company’s platform integrates with leading-edge algorithms dedicated to insurance pricing that can immediately spot anomalies and discover new patterns using which models can be built ten times faster than with traditional solutions, enabling insurance carriers to improve their profits and win market share with pricing models created and updated in hours instead of months.

DynaRisk: The company combines personal risk factors with external data and algorithms to determine an individual’s level of risk online, which can be used by the insurer to drive sales and by the policyholder for risk management.

Unqork: A no-code enterprise application platform that helps companies build, deploy, and manage complex applications, including insurance apps.

Instanda: A SaaS insurance software platform that allows insurance companies to build, configure, and launch products online.

Cytora: A service that transforms underwriting for commercial insurance. The Cytora Risk Engine uses artificial intelligence to learn the patterns of risks over time, enabling insurers to underwrite more efficiently and deliver fairer prices to customers.