We previously introduced the concept of Fintech Enablers, where companies provide financial services to then be distributed by non-financial companies, in this article. In this piece, we’ll be continuing onto the last part of the series. Sure, it’s not the sexiest part of embedded finance, (that title probably goes to Banking-as-a-Service, AKA BaaS), but it’s arguably the most important service these FinTech Enablers provide: Compliance-as-a-Service and Custody-as-a-Service.

Embedded Finance Part VI: Compliance-as-a-Service and Custody-as-a-Service

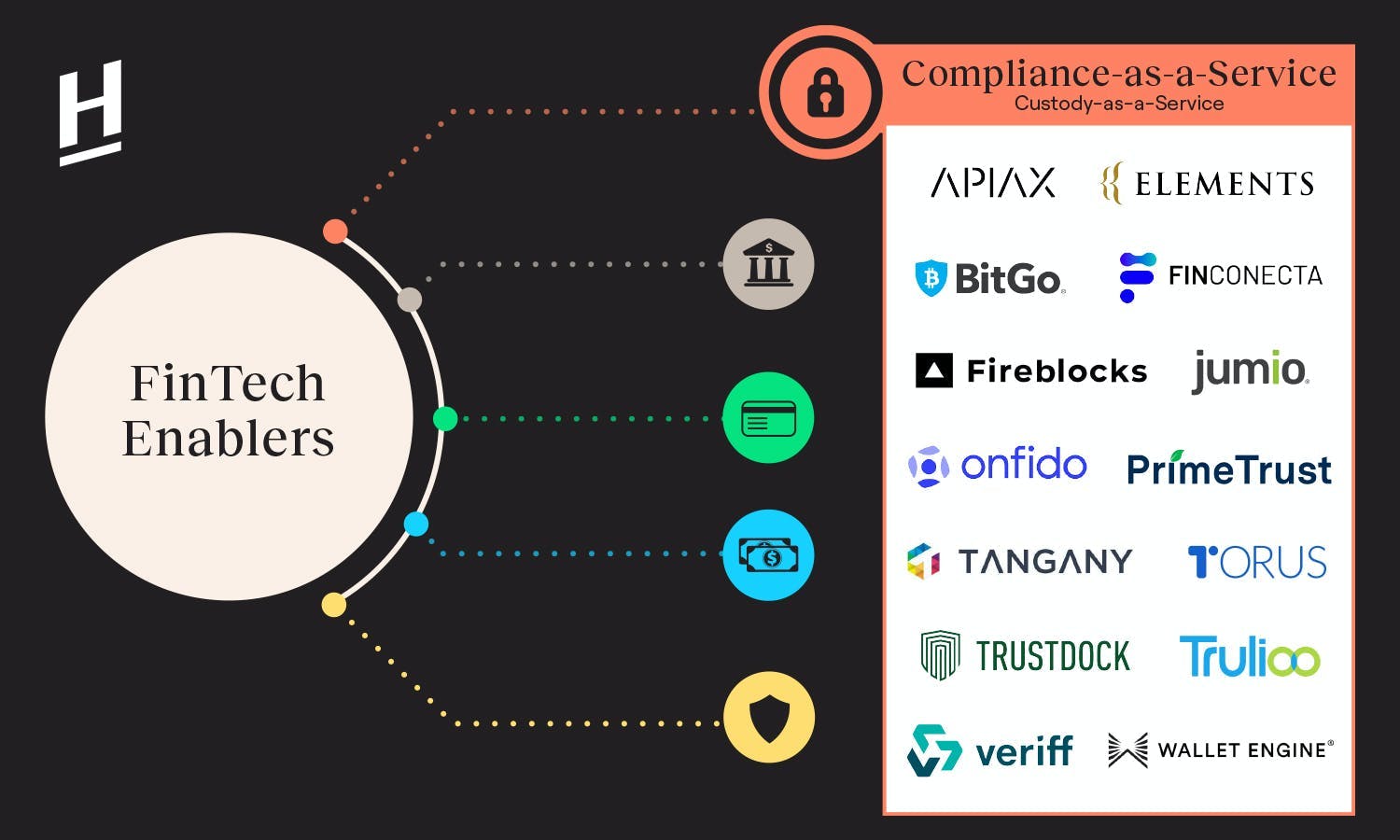

FinTech Enablers

What to Know About Compliance

When it comes to talking about compliance, it all boils down to this central question: Why do consumers trust their money with financial institutions and why do governments and regulators trust the financial institution to properly handle consumer assets? Because financial institutions are heavily regulated and require compliance to all kinds of rules and laws, which make sure they toe the line when providing their financial services.

Here are the four types of compliance requirements that most financial institutions need to deal with:

Know Your Customer (KYC): KYC ensures financial service providers know detailed information about their clients’ identity, risk tolerance, investment knowledge, and financial position. KYC protects both clients and service providers. Clients are introduced to products that best suit their personal situations. Service providers know exactly who their clients are, and thus generate and recommend the right products to the right person.

Anti-Money Laundering (AML): AML prevents criminals from disguising illegally obtained funds as legitimate income. The purpose, of course, is to reduce crime in society.

Counter Financing of Terrorism / Combating the Financing Terrorism (CFT): It might go without saying but a financial institution caught financing terrorism would have disastrous repercussions.

Data privacy: The most famous example would be GDPR. This set of laws regulates how service providers should handle the personal data that could be used to identify individuals.

Image courtesy of Trulioo

Compliance in the Past vs. Compliance-as-a-Service

In the past, financial service providers needed to build their own back office team to check that every transaction and every daily action happening in the company was compliant. In many countries, the regulators don’t allow for such work to be outsourced.

More importantly, compliance-related actions used to be legally required to be performed physically in person. In recent years, with a wave of loosening regulation that allows e-KYC (i.e., KYC performed digitally) and to some degree of outsourcing of such work, there are more and more startups that aim to assist financial service providers to handle KYC, AML, CFT, and other compliance-related tasks remotely.

Image courtesy of Onfido — document capture

One example is Onfido. Founded by three Oxford University students in 2012, Onfido has raised more than USD $180 million in funding from investors like SBI, TPG, Augmentum, and Salesforce Ventures. They provide sets of SDK and API to clients like Uber, Revolut, and BBVA that enable them to perform KYC within their own app.

Onfido competes with other players in this field such as Jumio (raised more than USD $200 million), Veriff (backed by Accel and IVP), and Trulioo (raised more than USD $400 million in funding).

In Japan, there are companies that also enable their clients to perform KYC digitally, such as Trustdock and ELEMENTS.

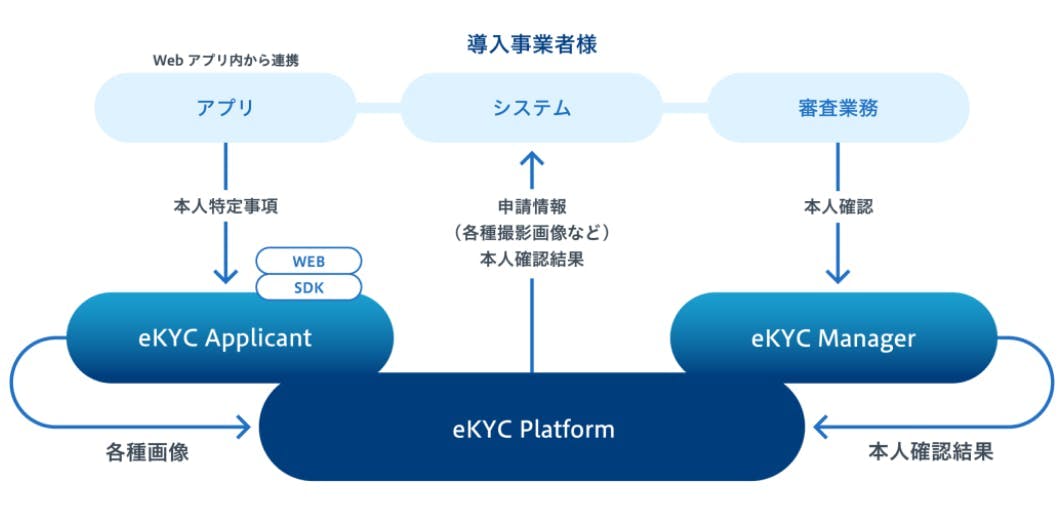

eKYC applicants provide their information via applications. eKYC managers check the information about the applicants. Companies can integrate the eKYC platform that links between eKYC applicants and eKYC managers.

Custody in the Finance Industry

Returning to our original question: why do we trust our money with financial institutions? The answer is that it’s less likely that a financial institution will lose its assets. Custody service is provided by custodians, who hold customers’ securities and other assets for safekeeping to prevent them from being stolen or lost.

It’s a boring job, but it is an important one. A custodian is usually a bank or an institution whose only service is to hold assets. Another way to call it, especially in the crypto world, is a wallet provider, in which case the assets are being held in digital “wallets”.

Custody-as-a-Service and Wallet-as-a-Service

When it comes to Custody-as-a-Service, there are two particular players that are worth mentioning.

- Prime Trust: Starting in 2016, Prime Trust has raised one of the largest Series A in this field. Prime Trust provides B2B custody, escrow, compliance, fiat processing, transaction software, and other services. The firm’s customers include crowdfunding portals, broker-dealers, investment advisers, crypto exchanges, securities ATS’, real estate syndicators, financial institutions, and next-generation financial application innovators. Prime Trust sets the industry standards for custody, fiat processing, escrow, and KYC & AML compliance with its frictionless API technology infrastructure which automates these processes. It competes with another giant in this field, BitGo.

- Fireblocks : Founded in 2018, Fireblocks has raised more than USD $480 million in funding. They reached unicorn status in less than three years. Fireblocks offers more than 500 clients an all-in-one platform to run a digital asset business, providing them with infrastructure to store, transfer and issue digital assets. It faces competition from smaller players such as Torus, Tangany, and Wallet Engine by Mambu. The big difference between the custody in the traditional finance world and the crypto world is, the latter focuses on how to store and manage the private keys, which could access the wallets.

Learn more

If you are interested in Fintech Enablers, check out our Intro to FinTech Enablers & Embedded Finance article.